Securities Lending - An Overview

A generally overlooked segment of capital markets, securities lending is a large and growing industry with interesting trading infrastructure opportunities

Securities lending is one of those areas we don’t hear much about but plays a critical role in capital markets. Its primary purpose it to support short selling trading activities, whereby short-sellers need to borrow securities to cover their short positions. It also enables securities holders to generate additional profits from those securities they loan out. Securities lending is key to supporting market efficiency and stability. Market participants rely on these transactions to meet liquidity needs, facilitating market-making.

The market for securities lending is sizeable; it is estimated there is currently ~$3.2T of securities currently outstanding on loan. Securities lending is one of the few remaining parts of capital market that operates in ‘the shadows’ with no real organized exchange (~60-70% of trades are happening offline), no central trading marketplace or central order book. This absence of centralized reporting (market and pricing information not widely disseminated across participants) drives significant information asymmetry, lack of transparency, and ultimately trading inefficiencies.

We’re seeing some interesting tailwinds in this space including growth in retail investor involvement, hedge funds shoring up demand, and recent increased accessibility to this market with electronification and new tools. In addition, recent regulatory actions could potentially introduce significant changes in the transparency of the market (e.g. SEC Rule 10c-1a ‘Securities Lending Rule’). This leads to interesting opportunities in next-gen trading solutions, data analytics, and ops/compliance.

General Overview

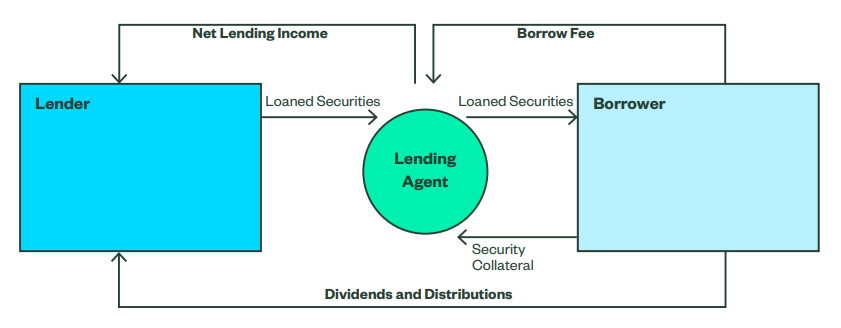

A securities lending transaction is the process by which one party (the lender) lends out and gives legal title to a security to another party (the borrower) for a certain period of time. The borrower will pay a fee to the lender for the use of the loaned security and will also post collateral for the transaction (cash or securities collateral).

Participants: there are usually four parties involved in a securities lending transaction: 1) the lender/beneficial owner, 2) the lending agent/custodian, 3) the borrower, and 4) primer broker

Lender: these are the beneficial owners of the securities that are being lent out (i.e. the supply side). It can include a number of players: pension funds, mutual funds, insurance companies, ETFs, sovereign wealth funds, and retail investors (through consumer broker/dealers).

Borrower: these are the borrowers of the securities (i.e. the demand side) that need to borrow those securities for their trading activities and strategies. It can include: hedge funds, broker/dealers, and more recently retail investors that engage in short selling activities.

Intermediaries

Lending Agents/Custodians: they will act on behalf of the lenders and play a key role in the execution and management of the securities lending trade. This can include custodians (i.e. BNY Mellon, State Street), large banks (e.g. Goldman, MS, JPM, BofA, etc.) - also prime brokers (see below), specialized lending agents (e.g. BlackRock), or broker/dealers (e.g. Apex). Their main tasks will include

Aggregating securities supply/inventory for location

Receiving orders from the demand side and performing stock locate activities

Underwriting and pricing the loans

Custody of the security and transaction collateral

Dealers & Prime Brokers: they will intermediate between borrowers and lenders. They will work with funds that want to borrow securities by identifying the securities or lending their own securities. They can also perform tasks such as obtaining the collateral required for the transaction from the borrower

Primary Drivers of Securities Lending

For Security Lenders - it is primarily for additional revenue generation as well as portfolio optimization

Lending Revenue: it allows lenders to generate additional revenue from lending their inventory of securities

Financing Requirements: lenders can also engage in lending their securities against cash

For Security Borrowers - it is primarily to execute on their trading strategies, mostly short selling, where they need to borrow securities

Short Selling: when a fund looks to go short on a position, they will need to borrow securities to cover that short position, and use the borrowed securities to settle a sale.

Other Strategies: the reason funds borrow securities can also be linked to other strategies. Proxy voting is one, where funds will want to accumulate a significant amount of securities prior to a transaction for voting purposes (i.e. empty voting). Other common ones can be merger arbitrage or convertible bond arbitrage.

Revenue and Fees

Lending Revenue: lenders will earn lending revenue from the borrower for the securities lent out. The lending rate/fee will vary significantly depending on the securities: easy or hard to borrow securities (i.e. scarcity), level of demand, counter-party, etc. The lending revenue is generally split between the lending agent/custodian/prime broker and the beneficial owner of the securities. The revenue share will vary significantly depending on the relationship between the parties. Lending agents will typically retain ~30% of the net revenues and the remaining ~70% will be for the lender/beneficial owner.3

Transaction Collateral: to mitigate the risk of a borrower not returning the securities, the lender will require the borrower to transfer collateral to the lender/lending agent

Most securities lending transaction are 1) fully or 2) over-collateralized

The collateral posted can be 1) securities or 2) cash. The vast majority of securities lending transactions in the US are cash collateralized (in Europe securities collateral is more prevalent). If cash is transferred as collateral, lenders will earn interest by re-investing that cash in money markets but will also pay a rebate to the borrower (the more in demand a security is, the lower the rebate).

Transaction Flow Overview: a typical securities lending transactions involves a number steps, systems, and manual interventions. The transaction is initiated by the demand side (i.e. hedge fund) who wishes to borrow a security to execute their short transaction.

Fund (or their broker) will reach out to the prime broker/lending agent with their request. The lending agent will then need to do a stock locate → process by which they see if they have inventory for the securities requested, in their own inventory or their customers’

Funds will send requests through FTP files, through broker portal, or via call/email

Lending agents will locate inventory through in-house system or 3rd party systems like FIS Loanet that aggregates available stock inventory (see ‘Tools & Infrastructure’ section below)

Once the lending agent/prime broker has confirmed the stock locate, they will quote the fund on their transaction including primarily lending rate/fee and collateral requirement

In order to determine the lending fees, lending agents/brokers will leverage data analytics platform such as FIS LendingPit or Data Explorers (acquired by IHS Markit and eventually S&P Global)

Once the transaction terms are agreed, both parties will execute the transaction which will settle at the DTC

Some electronic venues like Equilend have created marketplaces/trading platforms where parties can face each other and trade electronically. These platforms are primarily for general collateral (i.e. easy to borrow securities generally in large block trades). Hard to borrow securities (e.g. Siri, AMC, etc.) will not be traded on platforms like Equilend but rather manually broker to broker

Once the transaction is executed a number of operational steps will happen: transfer of collateral, booking of transaction in parties’ internal systems, and transaction reporting

Following the transaction, the position needs to be managed including daily mark-to-market valuation

Market Size and Recent Trends

Market Size and Recent Trends

Securities on Loan: there is an estimated ~$3.2T of securities on loan (a growth of ~28% since 2021), from a total pool of ~$38T of lendable securities. It is estimated that the US share of global activity in the securities lending space is ~58%.4

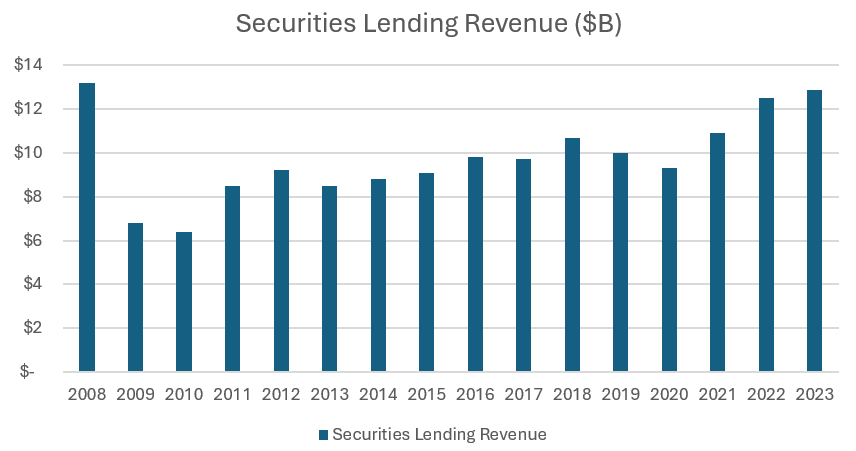

Securities Lending Revenue Opportunity: Annual revenue generated from securities lending transactions was ~$13B in 2023, that represents an increase of ~9% and ~16% from 2022 and 2021, respectively. The average blended lending fee in 2023 was ~50bps.7

Trends and Growth Factors: the industry fell significantly during and after the financial crisis of ‘08. There was significant short-selling scrutiny from regulators that put a hamper on demand from funds. A lot of those funds also exited the securities lending market after ‘08. In addition, during the ‘08 crisis, participants incurred significant losses on cash reinvestment programs (i.e. with risky investments) which led to participants revising their collateral management policies and more conservative cash reinvestment program. Finally, a cycle of persistent low interest environment following the crisis impacted the reinvestment of cash collateral (i.e. diminished incentives with low yields).

The securities lending market has recovered and grown in the past few years. A number of factors have led to this growth and tailwinds for the securities lending industry going forward:

Retail Participation: with the rise of the retail investor in the market, we are seeing a boom not only on the supply side for retail brokerage platforms, but also demand from retail investors now involved in short selling. The growth since Covid and the ‘meme stock’ craze is now an entrenched part of the market. Securities lending has become a significant revenue segment for retail brokerage platforms and they are actively promoting stock lending programs to users (e.g. IB Stock Yield Enhancement program9 or RobinHood Stock Lending program10).

Hedge Funds Growth: continued growth in the hedge fund industry and activity is shoring up demand for securities to be borrowed.11

Underlying Infrastructure: recent infrastructure advancements has made this space more accessible and expanded the pool of participants. We are seeing more on-ramps and electronification of the securities lending space (e.g. solutions like Equilend paving the way for electronic marketplaces). The electronification of the equities market and recent growth in electronification of the FICC space have also been a tailwind for the securities lending industry

Challenges with Existing Players: the largest incumbent solution in the electronic trading space, Equilend, is facing challenges including high fees, a lawsuit centered around anti-competitive behavior against new entrants in the space12, and is also about to be sold off13. This opens up the door for challengers with new and innovative solutions.

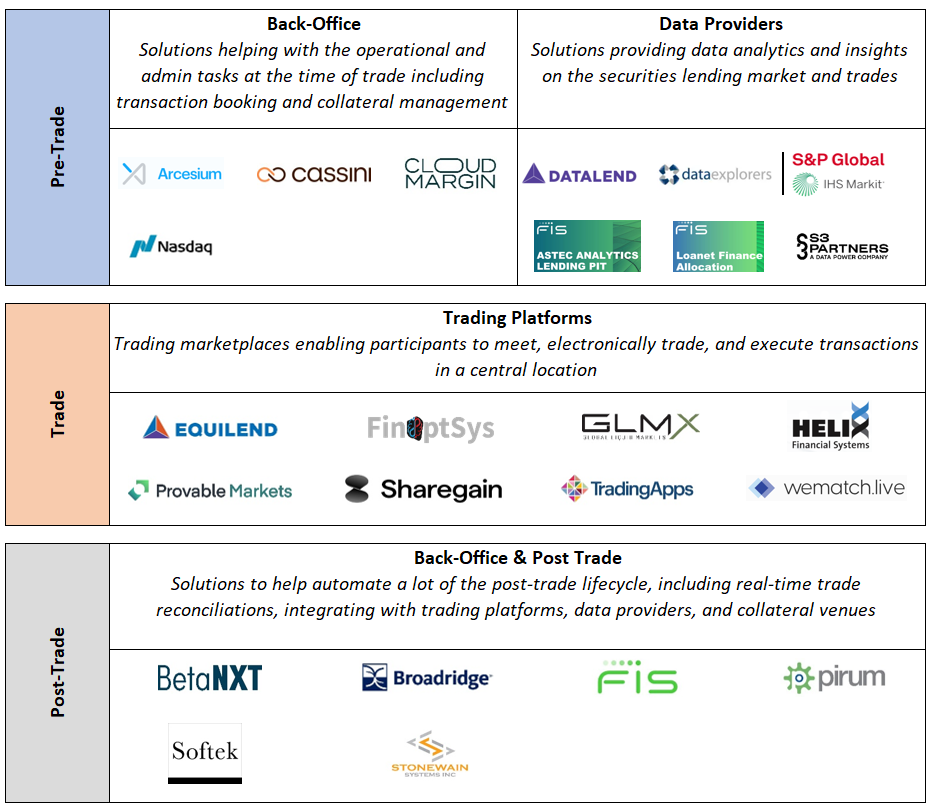

Securities Lending Tools & Infrastructure

Pre-Trade

Data providers will help participants in the securities lending transaction with valuable data to support trade. Stock inventory aggregation is very valuable to easily perform stock locate functions. Data analytics platforms will then mine the available data to provide insights to parties: trends on lending rates, utilization rates, benchmarking, performance, etc.

FIS Loanet is a main player in the inventory aggregation space (and back-office as well). Brokers will integrate with Loanet, push daily feeds of stock inventory, and will then give permissions to all other firms to see and access that inventory. That provides visibility on available inventory for lending agents interacting with borrowers

FIS Lending Pit, Data Explorers (now S&P Global/IHS Markit), and Datalend are key players in the data analytics space. Given the lack of organized and centralized exchange, these solutions play the role of data aggregators. They solve problems related to price transparency and trade data visibility. They will mine trading activity and give insights into trades, lending rates, utilization rates (supply and demand for certain securities), benchmarking trades against market, etc. This allows participants to evaluate markets, their own trades, how their lending agents are performing, how other lending players are doing.

Pre-Trade Management

Main function such as collateral management (pre-trade analysis, valuation exposure and changes) as well as automating of the trade booking

Main players in this space are Cassini, Calypso (now Nasdaq), and FIS

Trade Execution

Trading marketplaces provide a centralized location where parties can face each other, negotiate and execute trade. They become aggregate sources of liquidity for the market and facilitate better price transparency and more seamless trade execution. Price transparency is a big issue in a market like securities lending that does not have central marketplace; securities loan will get quoted very different fees by different parties. These trading marketplaces support primarily general collateral trades (i.e. for easy-to-borrow securities). Hard-to-borrow securities are mostly still traded offline

Equilend is the main trading platform in this space, and their NGT product. The platform is owned by a consortium of 10 large banks

Post Trade Management

These solutions help automate a lot of the post-trade lifecycle. Key functions will include real-time trade reconciliations, integrating with trading platforms, data providers, and collateral venues. Helping value the position with changing market rates, mark-to-market accounting, billing/accounting, and trade settlements. Primarily value of helping reduce operational costs of trade maintenance.

Pirum, FIS, and Broadridge are main players in this part of the stack

Notable Challenges & Opportunities

Data Transparency and Trading Automation

Securities and trading data in the securities lending space is currently primarily disseminated via a ‘give-to-get’ model, whereby participants provide information to data providers who aggregate and mine that data (e.g. Data Explorers, FIS LendingPit). This approach has two primary issues: not everyone submits their data and not every participant has access to the data. The problem is even more acute for hard-to-borrow securities where pricing/trading data can be very scarce and lack of clear information on cash collateral. In addition to general visibility, this leads to significant pricing inefficiencies where the same trades could sometimes get widely different prices/quotes.

Most securities lending transactions are still executed offline vs. on electronic trading platforms (e.g. Equilend, Wematch.live). Equilend NGT, the largest marketplace, has ~$120B of notional traded on the platform daily.14 The existing platforms are primarily focused on easy-to-borrow securities vs. hard-to-borrow securities. These trading platforms only cover a fraction of the market. In addition, existing electronic platforms are primarily there for participants to face each other, negotiate and accept trades; they are not real ‘matching engines.’

Post-trade management lifecycle is often burdensome and involves operational costs for participants driven by a fragmented toolset. From executing the trade, to booking it, reconciling the positions daily, tracking/mark-to-market the positions daily, and also managing the collateral.

Opportunity: a new type of trading platform where traders can meet and get matched. A trading marketplace that mirrors more of an exchange with a central order book. This could drive price and liquidity discovery, liquidity aggregation, and also automation in the trade matching and execution. Ultimately growing the pool of participants in this space.

Interesting company in this space: Provable Markets

Building an integrated, full stack ATS with trading and post trade solutions for securities lending. On the trading side, offering a central order book to consolidate supply and demand giving traders real-time view into activity and pricing, as well as direct connectivity to DTC/NSCC for trade settlements. On the post-trade side, the solution eliminates a lot of the hurdles and operational inefficiencies with straight through processing of transactions (API integrations into existing back-office systems, system is flexible to support existing back-office providers) for reporting and billing.

Compliance and Reporting:

SEC Rule 10c-1a ‘Securities Lending Rule15’ - new rule adopted by the SEC in 2023 that will require certain terms of securities lending transactions to be reported to a registered national securities association

The intended goal of the SEC regulation is to increase transparency in the securities lending space, by having to report information such as name of issuers, aggregated loan activity by security, and rates/fees/rebates for the loan

Market participants have already expressed some concerns about this rule including risks of information leakage regarding positions of short sellers and their strategies

Opportunity: this new rule will increase the compliance requirements for all participants. There is an operational opportunity to create systems and solutions to address these new requirements, workflow tools between compliance, legal and business units

S&P Global/IHS Markit via Federal Reserve Bank of New York and Financial Stability Oversight Council

S&P Global/IHS Markit via Northern Trust